Introduction

Picture this: you pull into a petrol station, glance at the price board, and feel that familiar sinking feeling. Your weekly shop costs a little more than last month. Your mortgage renewal letter arrives with a number that makes you pause. These are not isolated frustrations. They are the ripple effects of a conflict unfolding thousands of miles away in the Middle East.

Since hostilities between Israel and Iran escalated into open conflict, global markets have been rattled. Oil prices have spiked. Shipping routes are under pressure. And financial analysts are quietly reaching for a word they hoped not to use again so soon: inflation.

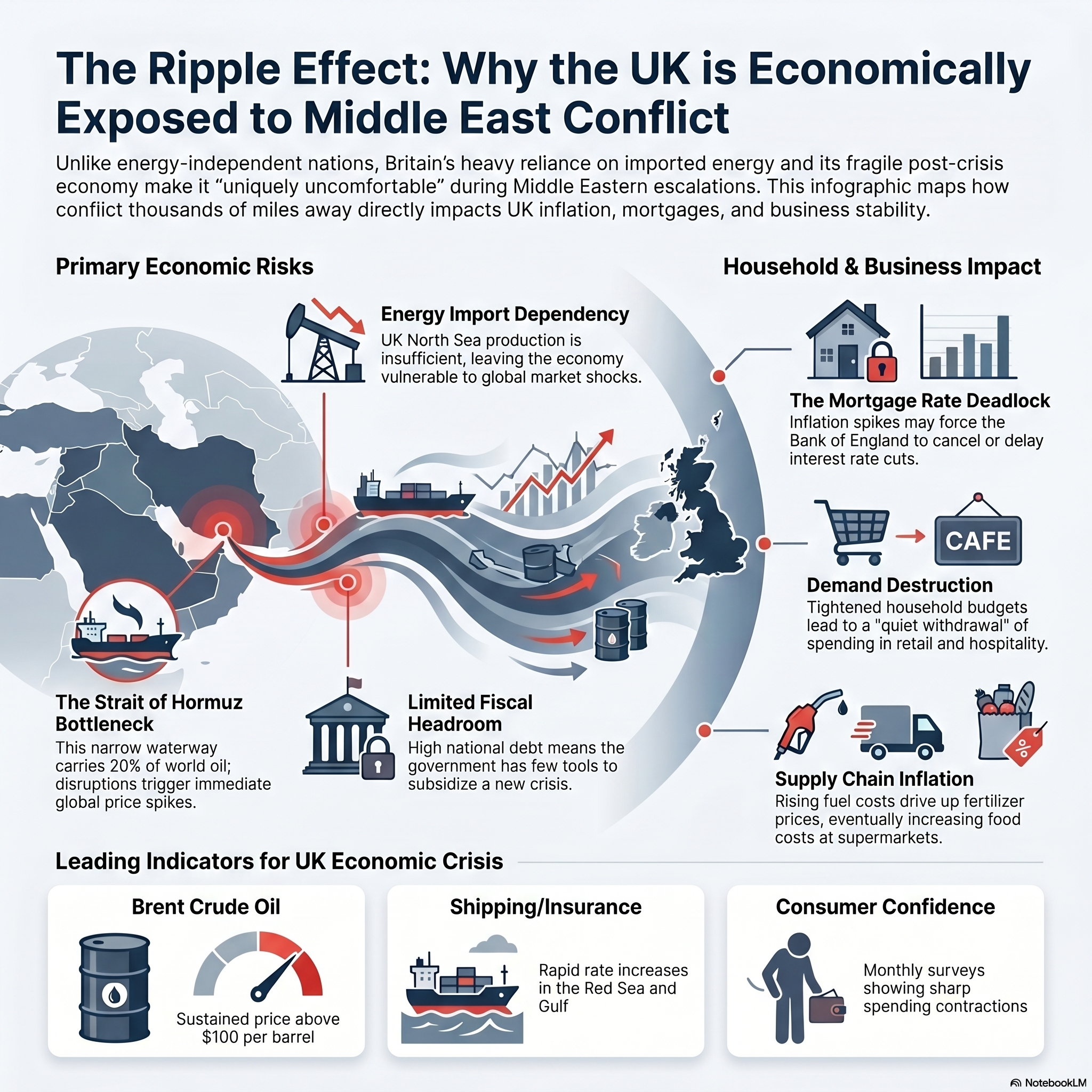

Britain, economists warn, sits in a uniquely uncomfortable position. Structurally dependent on imported energy, still carrying the scars of the 2022-23 cost-of-living crisis, and operating with limited fiscal headroom, the UK is, in the words of one senior market analyst, "particularly badly exposed" to whatever comes next.

Here is what that means for you.

Why the UK Is Economically Vulnerable

To understand Britain's exposure, you first need to understand where its energy comes from.

Unlike Norway, which produces its own oil and gas in abundance, or the United States, which has achieved near energy independence, the UK imports a significant share of the gas and oil it relies on. While North Sea production continues, it covers only a fraction of national demand. The rest arrives via global markets, which are deeply sensitive to geopolitical shocks.

That is where the Strait of Hormuz becomes critical. This narrow waterway between Iran and Oman carries roughly 20% of the world's oil supply. Any disruption there, whether from direct military action, Iranian threats to close the strait, or insurance-driven shipping avoidance, sends oil prices climbing on global exchanges within hours.

Higher oil prices do not stay in the oil market. They travel. They raise petrol and diesel costs. They push up the price of manufacturing and logistics. They eventually appear in your supermarket aisle and your energy bill.

For a country that never fully tamed inflation after 2022, the prospect of a fresh price surge is not merely uncomfortable. It is structurally dangerous. The Bank of England's credibility depends on keeping inflation near its 2% target. A sustained oil shock could force policymakers to abandon planned interest rate cuts, or worse, raise rates again.

How This War Is Hitting Household Finances

Fuel costs are the most immediate pressure point. Petrol prices are directly tied to the Brent crude oil price. When oil rises by $10 per barrel, a modest move in conflict conditions, pump prices in the UK typically follow within weeks. For households already managing tight budgets, this is money that disappears from somewhere else.

Food inflation is the second wave. Food production and distribution rely on fuel. Fertilisers are derived from natural gas. When energy costs rise, food prices follow, a pattern British shoppers experienced painfully between 2021 and 2023. Analysts warn that a sustained conflict could reignite food inflation at a point when many families have not yet recovered from the last episode.

Mortgages are perhaps the most politically charged pressure point. After years of rate hikes, millions of UK households were banking on the Bank of England cutting rates through 2025 and 2026. If inflation rebounds due to an oil shock, those cuts slow down or stop. Homeowners coming off fixed deals face the prospect of higher monthly payments, potentially for longer than anticipated.

Travel disruption adds further strain. Airlines flying routes through Middle Eastern airspace have already begun rerouting flights, adding hours and cost. Holiday prices are creeping upward. The summer travel season, which is economically important to UK consumers, faces real turbulence.

Business and Investment Risks

When household finances tighten, consumer spending contracts. Retail, hospitality, and leisure sectors, already navigating elevated costs, face the prospect of customers spending less. This is what economists call demand destruction: not a dramatic collapse, but a quiet withdrawal of spending that slowly drains growth.

Business confidence, meanwhile, is a fragile thing. Investment decisions get deferred. Hiring slows. Companies operating with thin margins begin looking at headcount. The housing market, which had shown tentative signs of stabilising, faces renewed uncertainty as mortgage affordability tightens and buyer sentiment softens.

For small and medium-sized businesses, the backbone of the UK economy, energy cost uncertainty is particularly damaging. Many negotiated fixed energy contracts during the relative calm of late 2024. When those contracts expire, renewal in a high-price environment could prove devastating for margins.

Foreign investment into the UK, already sensitive to political and fiscal signals, may also pause. Uncertainty, in investment terms, is always priced negatively.

Political Pressure and Social Unrest Risks

Britain's political landscape is already under strain. The government, operating with limited fiscal space following years of high borrowing, has few tools available if a new cost-of-living shock hits. Renewed energy bill support, for example, would be extraordinarily expensive and politically difficult to justify after the scale of pandemic-era spending.

Public frustration, if prices rise again, could translate into protest and political pressure at a speed that catches Westminster off guard. The 2022 cost-of-living crisis produced significant public anger; a repeat, particularly if it feels preventable, could generate stronger reactions.

There are also deeper social fault lines. Communities already experiencing economic deprivation are disproportionately affected by fuel and food inflation. The political consequences of that disparity are not predictable or easily managed.

What Happens If the War Continues

The economic impact of a prolonged conflict follows a rough timeline. In the short term, covering the first weeks to months, oil prices spike and inflation expectations shift. Markets reprice interest rate paths. Sterling can weaken as risk-off sentiment builds.

Over the medium term, spanning six to eighteen months, sustained high energy costs begin feeding through to wages, contracts, and corporate pricing decisions. If inflation proves sticky, the Bank of England may feel compelled to hold rates higher for longer, slowing the housing market, investment, and growth.

In a worst-case scenario of escalation involving direct Western military involvement or a closure of the Strait of Hormuz, recession risk rises meaningfully. Goldman Sachs and other major institutions have modelled scenarios in which a major Middle East oil disruption could shave percentage points off UK GDP growth. That is not alarmism; it is prudent scenario planning.

The UK is not defenceless. But its room for manoeuvre is narrower than many would like.

What Readers Should Watch Next

Oil price movements are your leading indicator. Watch Brent crude. If it sustains above $100 per barrel, domestic price pressures intensify quickly.

Bank of England communications matter enormously. Any shift in language around inflation or rate cuts will signal how seriously policymakers view the conflict's economic fallout.

Government policy announcements, particularly around energy bill support or household assistance, will indicate how severe Whitehall considers the situation.

Shipping and insurance rates through the Red Sea and Gulf of Oman reflect real-world risk perceptions far faster than official statements.

Consumer confidence surveys, published monthly, will show whether public anxiety is translating into reduced spending, the surest early sign of economic slowdown.

Conclusion

Global conflicts have always reshaped local economies, but in an era of interconnected supply chains, digital financial markets, and energy dependency, the transmission from battlefield to kitchen table happens faster than ever.

The UK's exposure to the Iran war is not inevitable catastrophe. It is a calculated vulnerability: the result of energy import dependence, post-crisis fiscal constraints, and an inflation environment that never fully normalised. Whether that vulnerability becomes crisis depends on how the conflict evolves, how policymakers respond, and how resilient British households prove to be.

What is certain is this: the cost of faraway wars is no longer abstract. It appears on your petrol receipt, your energy bill, and your mortgage statement. Awareness is the first step toward navigating it wisely.

Comments (0)

Leave a Comment

No comments yet

Be the first to comment