The Refex Group IT raid, launched by the Income Tax Department on December 9, 2025, rapidly became one of the most high-profile corporate events of the year in India's financial and business circles. Within hours of the searches beginning, media reports flooded news platforms with sweeping allegations, causing immediate and severe damage to the company's stock price and investor confidence. However, when the official record is examined carefully through the company's SEBI-compliant disclosures, its public statements, and a landmark RTI response received in February 2026, the picture that emerges is considerably more nuanced and significantly more favourable to the company than the media narrative suggested.

This article provides a comprehensive, fact-based account of the Refex Group IT raid what happened, what was alleged, how the company responded, and what official documentation has since confirmed.

Who Is Refex Industries? Understanding the Company at the Centre of the Storm

To understand the significance of the December 2025 search operations, it is important to first understand who Refex Industries is and what it represents in India's corporate landscape.

Refex Industries Limited is a publicly listed diversified conglomerate headquartered in Chennai, Tamil Nadu, trading on both the National Stock Exchange (NSE) and the Bombay Stock Exchange (BSE) under the ticker symbol REFEX. The company was originally incorporated in 2002 under the name Refex Refrigerants Limited, focused primarily on the refilling and distribution of hydro fluorocarbon (HFC) refrigerant gases used in air conditioners and refrigeration systems. In 2013, following a period of rapid diversification, the company was rebranded as Refex Industries Limited to better reflect the breadth of its operations.

Today, Refex Industries is the flagship listed entity of the larger Refex Group a business conglomerate that describes itself as one of India's most diversified business houses, with over 23 years of operational history across a wide range of sectors.

The company's business verticals include coal ash handling and management, where it is recognized as one of India's largest organized players, handling over 50,000 metric tonnes of ash daily across more than 19 thermal power plants spread across states including Madhya Pradesh, Karnataka, Chhattisgarh, Bihar, and Maharashtra. Key clients in this segment include NTPC, Ultra Tech Cement, Adani Power, and ACC. Beyond ash handling, the company is active in solar power generation, coal trading, power trading, electric vehicle operations through its green mobility arm, bio-CNG production, medical technologies, pharmaceuticals, airport operations, and capital market services.

In its most recent full financial year, the company reported revenues exceeding ₹2,400 crore its highest-ever revenue milestone driven by significant expansion in its ash handling and energy segments.

The Search Operations: A Day-by-Day Account of What Transpired

The Income Tax Department launched its search operations at premises linked to Refex Industries and certain business associates on the morning of December 9, 2025. The searches were conducted simultaneously across multiple premises in Chennai and other locations, in accordance with standard income tax search procedures under the Income Tax Act, 1961.

Income tax searches commonly referred to as IT raids in media parlance are conducted when the department has reason to believe that a person or entity has concealed income or assets beyond what has been declared. Under the law, such searches can cover business premises, residential premises, and the premises of associates and intermediaries linked to the primary subject of the search.

The December 9 searches at Refex-linked premises continued uninterrupted through December 10, 11, 12, and formally concluded on the evening of December 13, 2025 duration of five days. During this period, Income Tax Department officers examined physical and digital financial records, documents, and assets at the searched premises.

Throughout this entire period, the company has confirmed on official record that all company officers, employees, and associates extended full cooperation to the Income Tax Department, facilitating unobstructed access to premises, records, and all information requested by the department.

The Media Storm: Allegations That Dominated Headlines

While the search operations were still in progress, media reports began emerging with significant claims about alleged financial irregularities. These reports, published across major business news platforms and amplified through social media, made sweeping assertions about the scale of alleged wrongdoing discovered during the searches.

Among the claims widely reported were allegations of unaccounted income exceeding ₹1,000 crore, bogus purchase entries amounting to over ₹1,100 crore purportedly related to coal procurement and ash handling contracts undisclosed equity investments of ₹382 crore from 53 individuals and entities including employees and close associates of the promoters, an undisclosed foreign investment of approximately $30 million in a Swiss pharmaceutical company, unexplained cash deposits routed through companies allegedly opened in the name of a promoter's driver, and lavish personal assets including a private jet valued at ₹37 crore, luxury cars worth ₹10 crore, and high-end watches valued at ₹4 crore.

These reports, many of which cited alleged Income Tax Department press releases or unnamed official sources, created a firestorm in financial markets and generated intense public interest. The allegations drew particular attention to Anil Jain, Refex Group's promoter, as analysts, investors, and market participants were left scrambling to assess the potential implications for the company's listed entity.

Stock Market Impact: Lower Circuit and 52-Week Lows

The market reaction to the media coverage was swift and brutal. Shares of Refex Industries Limited fell sharply to a 20% lower circuit, touching a 52-week low in a single trading session as panic selling overwhelmed buying interest. The company's market capitalization suffered significant erosion in a matter of hours a stark illustration of how powerful unverified media claims can be in disrupting investor sentiment.

Around the same time, the Securities and Exchange Board of India (SEBI) also imposed separate penalties on the company's Chairman and Managing Director and certain other entities in connection with an insider trading matter an unrelated regulatory action that nonetheless compounded the negative sentiment surrounding the stock.

Refex Industries' Official Response: Categorical Denial and Investor Reassurance

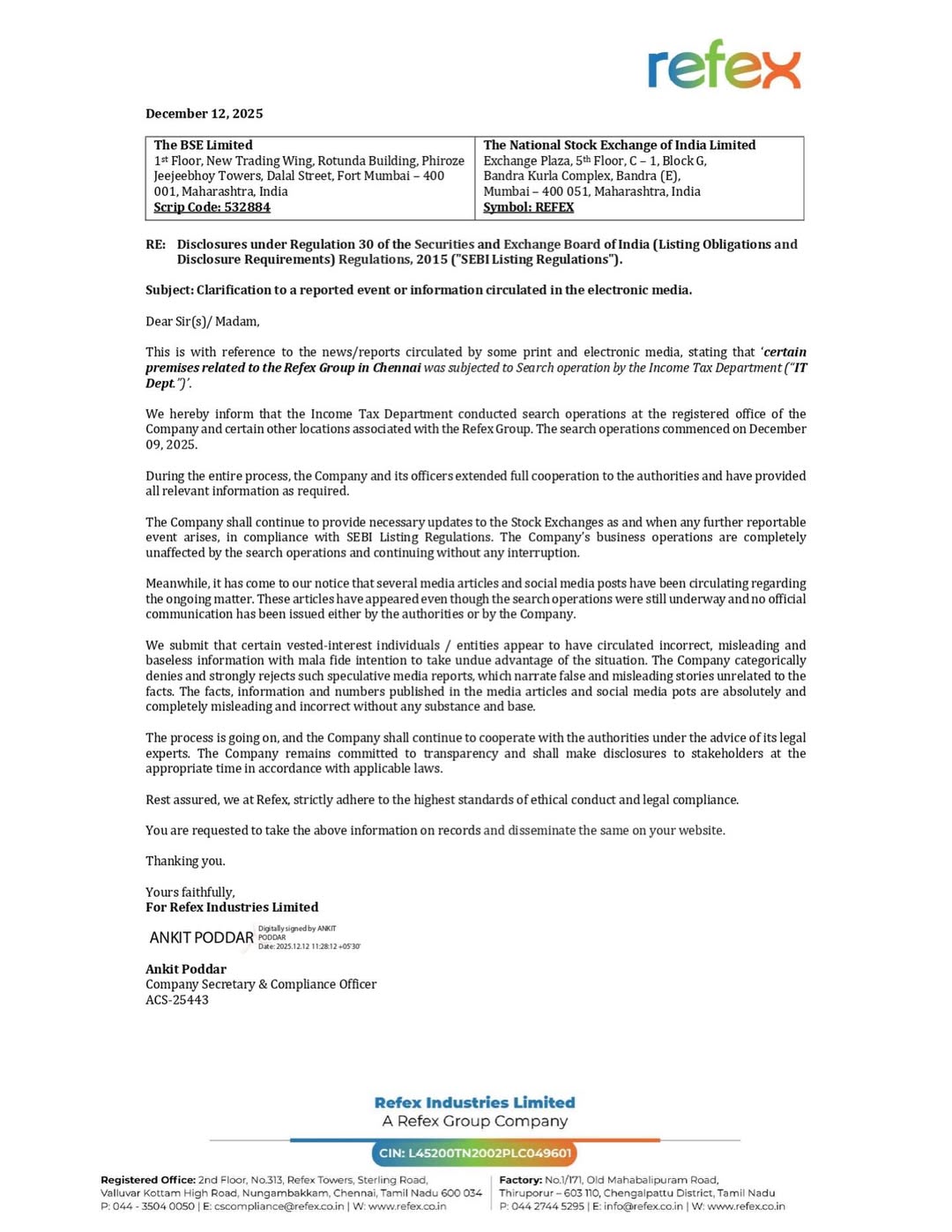

Even as markets reeled, Refex Industries moved quickly to issue an official response through the established regulatory channels. In a formal disclosure filed with the BSE and NSE under Regulation 30 of SEBI's Listing Obligations and Disclosure Requirements (LODR) Regulations, the company confirmed that search operations had commenced on December 9, 2025, and that the company and all its officers were extending full cooperation to the authorities.

More significantly, the company issued a categorical and strongly worded denial of the media reports. In its statement, Refex Industries described the reports circulating in print, electronic, and social media as "absolutely and completely misleading and incorrect without any substance and base." The company explicitly alleged that certain individuals with vested interests had deliberately spread incorrect and baseless information with malicious intent, seeking to take undue advantage of the situation to cause financial harm to the company and its investors.

The company categorically reassured its shareholders, investors, institutional partners, lenders, and business associates that all operations were proceeding normally and that the search process had not caused any disruption to its business activities. Ash handling operations at power plants, refrigerant gas distribution, solar energy projects, and all other business lines continued without interruption.

Conclusion of Search Operations: December 13, 2025

On December 14, 2025, Refex Industries filed a fresh official disclosure with the stock exchanges confirming that the search operations had formally concluded on the evening of December 13, 2025. This disclosure carried a point of critical significance: the company stated that as of the date of the disclosure, no adverse findings had been communicated to the company by the Income Tax Department, and that no formal notice, communication, or order indicating any adverse outcome of the search had been received.

Under India's income tax search framework, when the department identifies specific financial violations or demands arising from a search, it is required to issue formal documentation including notices under relevant sections of the Income Tax Act to the searched entity. The absence of any such formal communication from the department, as confirmed by the company in its official SEBI disclosure, represents an important factual marker in assessing the actual outcome of the search at that stage.

The RTI Application: Taking the Fight to Official Records

Unwilling to let unverified media narratives define public perception without challenge, Refex Industries took a proactive and strategically significant step: it filed a Right to Information (RTI) application with the Income Tax Department, specifically seeking to verify whether the department had issued any press releases, official statements, or public communications in connection with the December 2025 searches at the company's premises.

RTI applications in India allow citizens and organizations to seek information from public authorities under the Right to Information Act, 2005. Official responses to RTI applications carry the weight of government documentation and constitute part of the official public record.

The RTI Response: A Decisive Vindication

The RTI response, received by the company in February 2026 and dated February 10, 2026, provided an unambiguous and official confirmation: the Income Tax Department had not issued any press releases, official statements, press communications, or public-facing documents in connection with the search operations conducted at the premises of Refex Group and its associates in December 2025.

This RTI confirmation is of profound significance. It directly and officially contradicts the sourcing of several major media reports that had cited alleged Income Tax Department press releases as the primary basis for their sweeping financial allegations. With the RTI response now forming part of the official record, the credibility of those reports and the responsibility of their publishers is brought into serious question.

The episode highlights a critical issue in Indian financial journalism: media reports about income tax searches frequently cite alleged official sources that may not actually exist, and the absence of any mechanism for immediate verification allows such reports to cause enormous damage before the facts can be established.

What Responsible Financial Reporting Should Look Like

The Refex Industries episode serves as a case study in the dangers of uncritical financial reporting during sensitive regulatory events. Income tax searches are legitimate and important tools of tax administration. However, the reporting of such searches requires careful attention to what has and has not been officially confirmed by the department.

Key questions that responsible financial journalists should ask before publishing claims about IT search outcomes include: Has the Income Tax Department issued an official press release? Has the department provided official figures through verifiable channels? Has the company been given an opportunity to respond? Are the figures cited based on official documentation or on unnamed sources?

In the case of the December 2025 searches at Refex Industries, the RTI response has now established that the answer to the first question is definitively no the department issued no press release. This should serve as an important lesson for media organizations covering similar events in the future.

Business Resilience: Operations Continue Across All Verticals

Despite the turbulence of December 2025, Refex Industries and the broader Refex Group demonstrated significant operational resilience. Ash handling operations continued serving all 19-plus power plant clients without interruption. Refrigerant gas supply chains remained active across the country. Solar energy generation projects continued as planned. Electric vehicle and bio-CNG operations under the group's green mobility arm proceeded normally.

The group's management has consistently reiterated that the company's business fundamentals remain strong and that its long-term growth trajectory driven by expanding ash handling contracts, renewable energy investments, and diversification into new sectors remains intact.

Corporate Governance and Regulatory Compliance

Throughout the entire episode, Refex Industries fulfilled all its obligations as a listed entity. Every material development from the commencement of the search to its conclusion was disclosed to the stock exchanges in a timely manner in accordance with SEBI's LODR Regulations. The company's Regulation 30 disclosures are a matter of public record, accessible to any investor or analyst through the NSE and BSE disclosure portals.

The company's proactive use of the RTI framework to obtain and publicize official confirmation of the absence of departmental press releases further underscores its commitment to transparency and its willingness to engage with the official record rather than rely solely on reactive statements.

Conclusion: What the Official Record Actually Shows

The Refex group IT raid of December 2025 was a real event income tax search operations were genuinely conducted at the company's premises. However, the official record that has emerged in the months since the searches concluded tells a story that is considerably different from the media narrative.

No adverse findings were formally communicated by the Income Tax Department to the company. No official press releases were issued by the department in connection with the searches a fact confirmed by an official RTI response. The company disclosed all material developments to the stock exchanges in a timely and compliant manner. Business operations continued without disruption throughout the search period and its aftermath.

These are not merely the company's assertions they are matters of official documentary record. As investors, analysts, and the broader public continue to evaluate the Refex Industries story, it is these official records that should form the basis of any fair and accurate assessment.

Comments (0)

Leave a Comment

No comments yet

Be the first to comment