"For the first time since December 2022, the share of respondents expecting global conditions to worsen over the next six months is larger than the share expecting improvement." McKinsey Global Economic Conditions Survey, late 2025

The Signal the Markets Are Sending Is Not Subtle Anymore

Markets do not panic. They price. And what they have been pricing for the past several months, across equities, bond spreads, and commodity futures, is a world in which the probability of things going badly wrong is materially higher than it was a year ago.

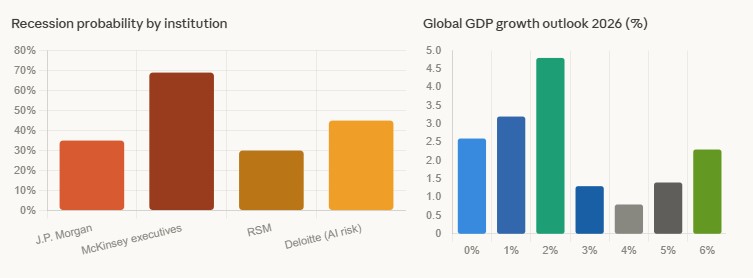

Global recession risk 2026 is no longer a tail scenario whispered about in trading rooms. It is a mainstream probability discussed at the highest levels of institutional finance. J.P. Morgan Global Research has placed the probability of a US and global recession in 2026 at 35%. McKinsey's global survey found that nearly seven in ten business executives now rank a recession scenario as the most likely outcome for the world economy, up from 53% just one quarter ago.

These are not fringe views. These are the considered assessments of the institutions that manage the flow of global capital. When they move their probability estimates upward together, it is worth asking what they are seeing.

"Rising Uncertainty Causes Consumer Confidence to Drop"

The Demand-Led Recession Risk Is the Most Dangerous Kind

The largest single concern among McKinsey survey respondents is not a financial sector collapse or a sovereign debt crisis. It is something more insidious: a demand-led recession, in which rising uncertainty causes consumer confidence to drop, spending contracts, businesses pull back on investment, and a self-reinforcing cycle of caution produces the contraction it was designed to avoid.

This pattern is particularly dangerous in 2026 because the two primary engines of consumer confidence over the past three years, rising asset prices and stable employment, are both under simultaneous pressure.

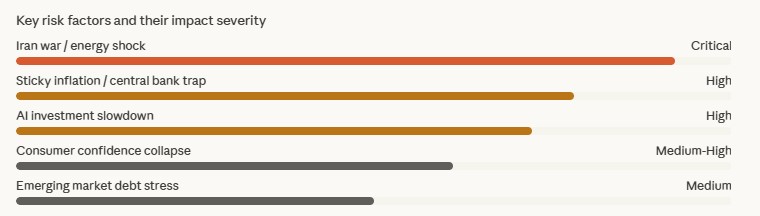

Asset markets have delivered prolonged volatility rather than the steady appreciation that sustained household wealth in 2021 and 2022. The Iran-US conflict has kept energy prices elevated and supply chains under pressure since February 28. Inflation that was supposed to be on a clear downward path is, as J.P. Morgan notes, "sticky," hovering around 3% with little sign of moving lower, and with upward pressure from trade war-related goods prices expected to persist through at least the first half of 2026.

The labour market picture is equally ambiguous. Goldman Sachs expects global GDP growth of 3.2% in 2026, but notes that "the job market outlook is less inspiring" because ongoing productivity acceleration from AI "raises the bar for how much GDP growth is needed to create jobs." In plain language: the economy can grow and employment can stagnate simultaneously. That combination, growth without jobs, erodes the consumer confidence that demand-led models depend on.

Three Fault Lines Running Through the Global Economy Right Now

War, Inflation, and the AI Valuation Question

Fault Line One: The Iran War and Energy Markets

The closure of the Strait of Hormuz, which carries roughly 20% of global seaborne oil, has been the most direct exogenous shock to the global economy in 2026. Brent crude surpassed USD 100 per barrel in early March, rising to a peak of USD 126 before partial relief from diplomatic negotiations. Energy price spikes of this magnitude feed into every downstream cost: manufacturing, logistics, food production, heating, and transport.

ING's risk scenario analysis explicitly lists war-related energy disruption as one of the most consequential downside risks for 2026, noting that higher energy prices produce "weaker global growth and higher inflation" simultaneously, forcing central banks into the impossible position of needing to both stimulate and restrain the economy at the same time.

Fault Line Two: Sticky Inflation and the Central Bank Trap

The global inflation story of 2026 is not a story of triumph. It is a story of incomplete victory. After unwinding supply shocks related to the pandemic and the Russia-Ukraine war, inflation has hovered around 3% with little sign of moving lower.

Central banks in the US, UK, and eurozone cannot cut rates aggressively without risking re-ignition of inflation. They cannot hold rates high without increasing the probability of recession. This is not a new problem, but it is a problem that has been going on long enough that the cumulative pressure on mortgage holders, small businesses, and household budgets is compounding in ways that early 2025 models did not fully capture.

Fault Line Three: AI as Singular Support and Singular Risk

Every major institutional forecast for 2026 contains a version of the same warning: AI-related investment is a significant driver of current growth, and a pullback in that investment would be enough to tip the balance. Deloitte's assessment is direct: "A drop in AI-related spending next year could be enough to push the economy into a recession. Other parts of the economy are more strained and will therefore not be able to make up for the loss."

ING identifies the same risk: if AI-driven consumer spending and business investment growth shift lower, GDP growth could turn negative in the first half of 2026. An economy with a single, concentrated engine of growth is fragile in a way that diversified economies are not.

The Countries That Will Suffer Most Are Not the Ones Making Headlines

Developing Nations Face Compounding Crises

The recession conversation in Western financial media is almost entirely about the US, Europe, and China. This framing obscures where the real human cost of a global downturn lands.

The World Bank's Global Economic Prospects report makes the vulnerability of emerging markets and developing economies explicit: "Risks to the outlook remain tilted to the downside, including those from renewed trade frictions and policy uncertainty, tighter global financial conditions, elevated fiscal vulnerabilities, rising geopolitical tensions and conflict, and climate and public-health-related shocks."

For low-income countries, real per capita income growth is projected to average only 2.8% in 2026 to 2027, which the World Bank notes "remains insufficient to recover pandemic-era losses or generate adequate job creation, leaving extreme poverty widespread."

Countries most exposed are those that depend on exports to China or the US, carry elevated debt burdens that limit fiscal response capacity, and face sizable current account deficits that make them vulnerable to capital outflows when global financial conditions tighten. In Latin America, sub-Saharan Africa, and parts of South and Southeast Asia, a global recession does not mean a quarterly GDP contraction. It means food insecurity, unemployment, currency collapse, and the reversal of years of development progress.

What Investors Are Actually Doing

Confidence Is Weakening at the Margin, Not Collapsing

It would be inaccurate to describe the current environment as one of investor panic. It is more precise to describe it as one of investor doubt: a shift from confident deployment of capital into growth assets toward a more cautious posture that demands higher risk premiums for uncertain outcomes.

Morgan Stanley's Seth Carpenter, Chief Global Economist, captured the current investment logic accurately: "These two factors, strength in consumption and business spending, were why we never called for a recession early in 2025, when markets pulled back on trade policy fears. The question now is whether those factors remain strong enough."

That conditional framing is precisely the problem. "Whether those factors remain strong enough" is a sentence that was not being asked in 2023 or early 2024. The fact that it is now the central question in institutional investment conversations tells you where market confidence actually is, even if headline indices have not yet reflected the full scale of that uncertainty.

RSM's US Chief Economist has reduced his 12-month US recession probability to 30%, down from 40%, on the basis of expansionary fiscal policies and rate cut expectations. That is not bullish. A 30% recession probability is a market where one in three professional observers thinks the economy contracts within a year.

The Question Nobody Wants to Answer Directly

Is a Recession Closer Than We Think?

The honest answer, based on the data, is: closer than the mainstream headlines suggest, but probably not imminent in the way the phrase "global recession" implies to most readers.

Goldman Sachs' baseline forecast of 3.2% global growth in 2026 is not a recession forecast. Morgan Stanley's base case sees growth moderating, not collapsing. J.P. Morgan's 35% recession probability means a 65% probability of avoiding one.

But none of those forecasts account for what happens if the Iran war escalates to include a ground offensive and the Strait of Hormuz remains closed through peak summer 2026. None of them fully price the possibility that AI investment, which has been the single most important driver of US growth for two years, plateaus or falls. None of them assume a sharp deterioration in consumer confidence driven by six consecutive months of energy-driven cost-of-living pressure.

The markets are not predicting a recession. They are pricing the possibility of one more seriously than at any point since 2022. That is not the same thing. But it is also not nothing.

An Expert's View: What Should Be Done

This Is a Moment for Policy Clarity, Not Policy Drift

Recessions that are preceded by prolonged uncertainty are often worse than recessions that arrive suddenly, because uncertainty itself causes the demand contraction that precedes the formal downturn. The period from now through mid-2026 is analytically the highest-risk window.

Three things could materially reduce recession probability between now and July 2026: a durable ceasefire in the Iran war that reopens the Strait of Hormuz to full shipping; a credible Federal Reserve communication strategy that manages both inflation and growth expectations without triggering a credit freeze; and a coordinated signal from the G7, which met in France on March 26 to 27, that fiscal policy will support demand in the event of a synchronised downturn.

None of those three things is happening clearly enough right now. That is the gap between where markets are and where policy needs to be. And it is why the question in this column's headline, whether a recession is closer than we think, does not yet have a comfortable answer.

Comments (0)

Leave a Comment

No comments yet

Be the first to comment